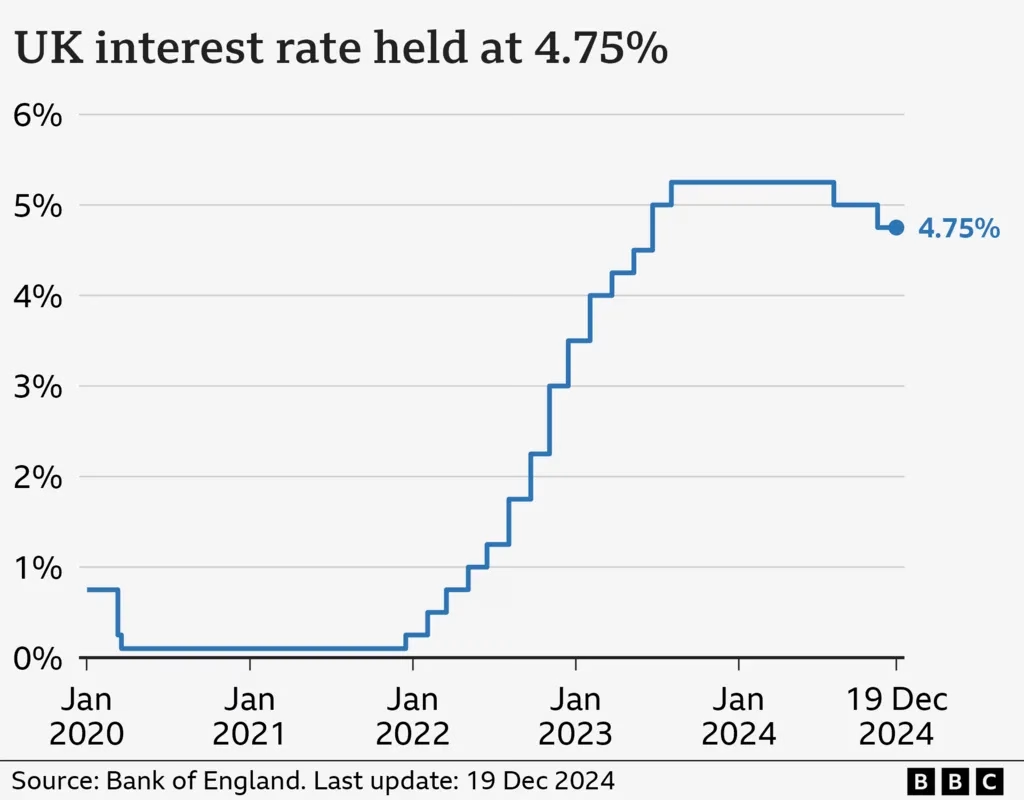

- UK interest rates held at 4.75%

- Rates expected to fall in 2025

- Mortgage rates may rise

The Bank of England has voted to keep interest rates unchanged at 4.75%, despite three members of the nine-member rate-setting committee advocating for a reduction to 4.5%.

The decision came as the Bank acknowledged that the UK economy had underperformed, with no growth recorded between October and December, falling short of expectations. Although interest rates remain steady, the Bank indicated that a gradual reduction in rates is expected next year, with the first potential cut possibly occurring in February 2025.

Bank of England Governor Andrew Bailey commented on the decision, stating, “We think a gradual approach to future interest rate cuts remains right, but with the heightened uncertainty in the economy, we can’t commit to when or by how much we will cut rates in the coming year.”

Recent data has shown inflation is still above the Bank’s target, while wages are growing faster than expected. However, the economy is facing challenges. The Bank had initially forecast growth of 0.3% for the final quarter of 2024, but now expects no growth at all for that period.

This downgrade in economic forecasts is seen as a setback for the Labour Party, which has made boosting economic growth its primary focus. Labour has pledged to achieve the highest sustained economic growth among G7 nations.

In the minutes from the meeting, the Bank of England noted uncertainty about the effects of the measures announced in the Autumn Budget. The Budget, introduced by Chancellor Rachel Reeves, included £40 billion worth of tax increases, most notably a rise in National Insurance contributions from employers.

The Bank’s next decision in February will be informed by more data on the impact of the Budget changes and on the potential effects of incoming US trade tariff policies under President-elect Donald Trump.

Chancellor Rachel Reeves commented on the Bank’s decision, saying, “We want to put more money in the pockets of working people, but that is only possible if inflation is stable, and I fully back the Bank of England to achieve that.”

Liberal Democrat Treasury spokesperson Daisy Cooper MP criticized the government’s approach, stating, “The new government needs to work much harder if it’s going to turn the economy around any time soon. That must start by scrapping the self-defeating jobs tax, which promises to make the crisis in health and care even worse.”

Ruth Gregory, Deputy Chief UK Economist at Capital Economics, noted that the Bank of England’s recent comments suggested policymakers were more open to cutting interest rates than expected, potentially signaling quicker cuts than investors anticipate.

Meanwhile, Danny McGuire, a 33-year-old from Warrington, Cheshire, expressed his frustrations with the high cost of housing. “The idea of owning your own home is preferable to renting for myself,” McGuire said. “But average house prices are incredibly high.”

Sarah Coles, Head of Personal Finance at Hargreaves Lansdown, warned that for those looking to secure a fixed-rate mortgage, the market’s uncertainty could lead to slight increases in mortgage rates. “Mortgage rates have fluctuated over the past month, as the market struggled to make its mind up about the path of future rate cuts. With so much uncertainty around, it can be a good idea for anyone with a looming remortgage to secure a rate now,” she advised.